Quick disclaimer – I started writing this article weeks ago, tabled it, and I just came across it again. Given that May is Mental Health Awareness Month, I thought it time to share. I know that this piece may seem a little off-topic from my more typical college planning advice, but I promise it’s not. So, please stick with me ’til the end and I promise I’ll step down from my proverbial soap box.

Anyhow, about a year ago I made a commitment to regularly remind my students about the importance of reading. Books, that is. NOT social media or their newsfeed on their mobile devices, but actual books (they could be eBooks or even audiobooks). I’ve become pretty adept at working, “What are you reading right now?” into most of my meetings with my students.

There are a number of reasons I want my students to develop an appetite for reading, and yes, many of them have to do with college (a proven link between reading and improved standardized test scores, the ability to craft a well-written, compelling narrative, conduct a conversation with an adult/admissions representative, facilitate independent performance in rigorous courses, etc.). But…there is more. To me, books, even those that don’t contain pointedly relevant material, are the impetus for ideas, can spark creativity, and improve articulation. Even the most obscure graphic novel can offer overt instructions for overcoming life’s obstacles.

So, I like books – to give them and receive them. And I just finished a really great one which has made me double down on my insistence that my students get to a library and start reading. Like right now and definitely, this summer!

It’s called The Anxious Generation, and it’s written by NYU professor Jonathan Haidt. It is both frightening and insightful, and frankly a must-read (imho) for every parent, educator, counselor and psychologist. Even students will find this book to be of interest, even if they may resist its recommendations.

The book examines the increase in anxiety and depression among Gen Z, or those born after 1995. This is the first generation to grow up in a world of social media and smart phones, or a phone-centric world, and the impact is, well, depressing. Reported rates of anxiety and depression rose remarkably between 2010 and 2015 (and continue), or the years that social media apps grew in popularity and use on smart devices. Haidt makes a number of interesting points, among them that we are very overprotective of our children in the real world, but extremely under-protective in the virtual world. We are super nervous about allowing our kids to leave the house alone, walk or ride to the corner store by themselves, or even engage in unstructured play out of fear that they will be approached by a predator, abducted, or find themselves in an uncontrolled, chaotic activity where grownups are not around to set the rules. Yet online, we give our kids full rein to access well, anything…extremism, hate, bullying, pornography, etc. And this exposure happens when our teens are not fully formed and their decision-making ability is inchoate at best. COVID only exacerbated this, and cobbled together, it all leads to more fear, anxiety and depression, low self-esteem, and a reduction in taking proper risks that can lead to growth.

I’m worried about our kids. So I’m thrilled when I hear an enthusiastic response to my question about reading, especially when that response includes not only a title (and author) but also a brief synopsis of what the book is about. Little tidbit – I usually go and read what they’re talking about and wind up having an ongoing, albeit small, book club with some of my students. On their recommendations (and on my own) I’ve read All the Light We Cannot See by Anthony Doerr, AlexanderHamilton by Ron Chernow, BenjaminFranklin by Walter Isaacson, American Dirt by Jeanine Cummins, My Effin’ Life by Geddy Lee, Poison Ivy by Evan Mandery, The Alchemist by Paulo Coelho among several others.

That said, the response I hear more often from students is, “Oh, I’m not reading anything right now”, followed by an excuse or rationalization such as “I have so much schoolwork to do”, or “I don’t have time with my busy schedule.”

For some kids who are overscheduled and overworked, I reluctantly accept that answer. For now. But once summer hits, I start calling bull$h!t and I’m going to start asking them how much time they spend on social media, watching Netflix or playing video games.

In 17+ years of counseling students I find that those kids who continue reading through high school are the ones who have the most success when it comes to competitive college admissions. I’m not saying kids need to read a book every month if they want to get into college, but on the most selective side of the admissions process, the readers are those who enjoy the most success.

Facts (for those sick of my opinion): kids who read more tend to outperform their peers on the SAT or ACT, which are mostly reading tests; their advanced skill and practice with words tends to make them more expressive and hence better writers, which often translates to better college essays; college interviewers often ask about books that students have read recently; and when students get to college they are more likely to succeed because they are already familiar with the rigors of heavy reading, which is a tough switch to simply flip on when the academic workload increases.

So, I’m asking my students — and encourage you to do so as well — “How much time are you spending on social media or playing video games each day?”

The answers so far don’t surprise, but they do concern. A typical response is “about 3-4 hours each day”. Haidt makes some good recommendations about how to reduce that…and I’m happy to discuss his suggestions with you privately. But returning to my main point – I’m trying my best to encourage my students to rekindle their interest in reading. I’m convinced that this activity leads to so many benefits that translate into success on the college admissions front, as well as making them better thinkers and better students.

If you share that philosophy, let us know what you’re reading…and check out our growing community at Your College Concierge of like-minded college planning advisors, educators, merchandisers, and college lifestyle experts. The journey from child to adult — not to mention to and through college — can be fraught with so many challenges, but together we can make that road a far more enjoyable adventure.

P.S. Whether your rising 12th grader is a reader or not, s/he will clearly benefit from our Summer Application Boot Camp. Click here to learn more and sign up!

P.P.S. At the risk of sounding hypocritical, follow us on Instagram @YourCollegeConcierge. Not all social media is bad!

P.P.P.S. Decision Day (May 1) came and went, and while many in the Class of 2024 have settled on a college home, many others are still awaiting financial aid offers that are delayed because of the FAFSA Fiasco. I will have more on Class of 2024 results in the week ahead.

There’s nothing quite like March Madness. To me, the sports fan, it’s without question the most exciting event of the year. Nearly every game comes down to the wire, leaving fans breathless and exhausted. It’s great – even for the most casual observer. But for me, the college counselor, it’s perfection.

For the past 17 years, the annual NCAA tournament has given me a chance to geek out and make picks based on a financial aid/institutional scholarship formula (a ‘University Generosity’ algorithm, if you will) that I’ve been keeping data on and tweaking for years. Now, full disclosure, you’re not likely to win your office pool with my picks, but it very well could pay off in the best possible way when it comes to your college tuition bills. Here’s how:

True, college is undeniably uber-expensive…on paper. The cost of attendance has been growing exponentially for years. Just 17 years ago when I first got started with this, the most expensive colleges cost about $56,000 all in; today those same schools (and quite a few others) have published cost of attendance north of $90K. Now before you hyperventilate, here’s the good news: very, very few people are expected to pay the full cost of attendance.

So, today’s tip:

IGNORE the sticker prices! The published prices are not the prices you should be paying. In fact, more than 2/3 of full-time, first year college students pay LESS than the sticker price. A lot less – the average discount rate, which is the list price less need-based and merit-based aid is at a whopping 56% (which is an all time high).

Colleges discount!! All of them. Just not for the same reasons, or to the same extent. Fact is – some colleges are more generous than others! Full stop. Colleges have two main instruments when it comes to their discounting strategies: 1) need-based Aid and 2) merit-based (or non-need based) Aid. Most schools utilize both tools — though certainly not in equal measure — to induce students to attend their institution. Without a doubt, the largest source of free money is in need-based Aid (more than $150 billion worth – yes, I said billion). It is a legitimate source of college savings for forgotten middle and upper middle class families (six figure earners), and choosing schools that offer substantial need-based grants is a critical component of my March Madness formula — and it certainly should factor into your Admissions strategy.

It’s my experience that most families don’t really know this and certainly don’t know how to determine which colleges will be ‘generous’ with them and for what reasons, or how to determine what % of that published cost of attendance they’ll be expected to bear (hint: this is a manageable number), or even how to apply for financial aid (actually 7 out of 10 don’t even know where to begin), much less understand the rules of the game. And, in this case what you don’t know can hurt you.

So, by analyzing the Men’s bracket and comparing the historical ‘generosity behavior’ of the colleges using my unique formula, I’m not only giving you a chance at an ‘out-of-the-box’ strategy to bust your family’s or company’s pool, but I’m also giving some invaluable insight into how schools in the tournament address and award financial aid and scholarships.

I’m not going to get into the intimate details of my secret sauce, but we focus on the financial aid generosity levels of each school, as well as average net cost. As I mentioned, most families who are “shopping” for college have little idea how much they should eventually pay because: 1. They don’t know their Student Aid Index (SAI); and 2. They’re not aware of the generosity history at the schools on their list. Knowing these two facts can help you pretty accurately ballpark your eventual NET annual expense per each school you’re considering. (Note: if you have any questions about the generosity of the schools on your list, please feel free to ask – with the right information, I can provide you with an accurate projection).

But for now, let’s break down this year’s bracket:

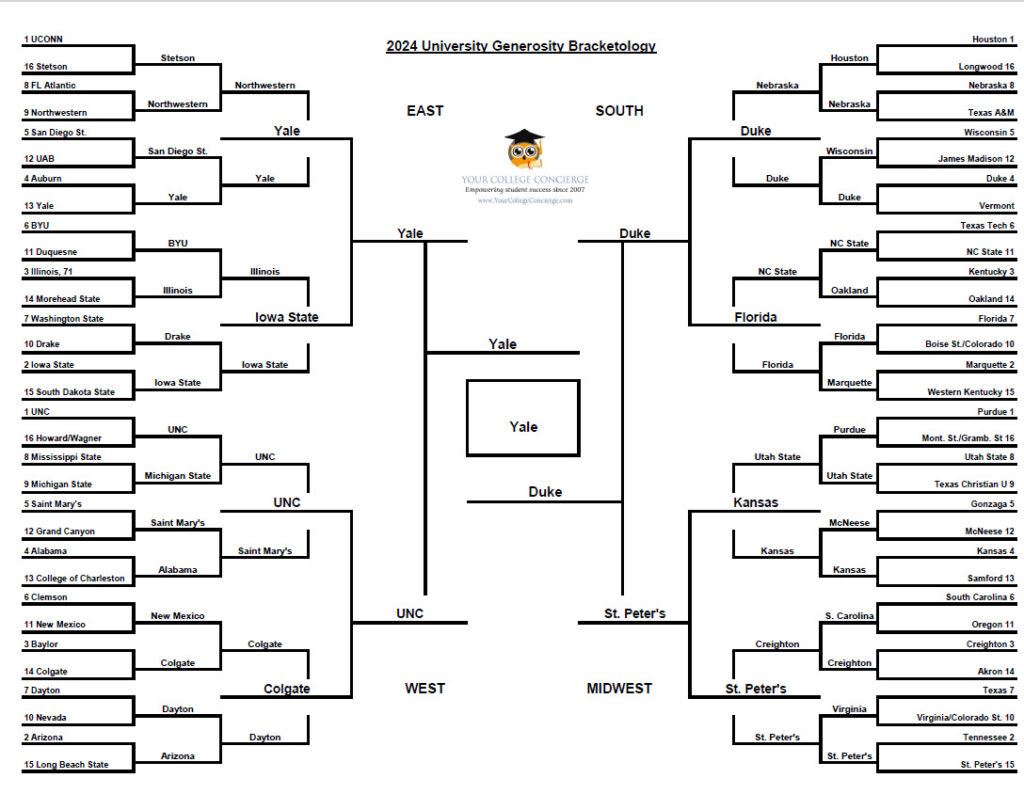

1. The East Bracket is loaded with generous schools: There are several gems in this quarter of the bracket, including Ivy League champion Yale, which statistically may be the most generous school in the entire field. Northwestern also meets 100%. Even lowly Stetson, seeded 16 and a first-time entrant to the Big Dance, meets 90% of demonstrated need so I have them over universal favorite and 5 time NCAA Men’s Champion (and defending champ) UConn. BYU may only meet 35% of need, but their very low sticker price gives them big points and makes them much more affordable.

2. Dayton is always a good Flyer: Not only does Dayton have a great basketball tradition and a strong aerospace program, but they’re pretty good at financial aid, too (89% of demonstrated need). They face a financially stingy Nevada (56% of demonstrated need), and then face off against Arizona, a basketball powerhouse that only meets 64%. What’s worse about Arizona, their average net price is $17,202 – quite high for a state school. I’m taking the Flyers.

3. Western Kentucky has no chance: This school is the financial aid doormat in this year’s bracket, meeting only 24% of demonstrated need. That’s abysmal, so don’t think twice about selecting 2-seeded Marquette to top the Hilltoppers.

4. St. Peter’s is my favorite Cinderella: This school shocked the nation two years ago with their improbable run, defeating powerhouse Kentucky in the first round (I also picked them then, when they were also a 15 seed) en route to an eventual Elite 8 defeat against financially generous (100%) UNC-Chapel Hill. More importantly, they not only meet 88% of demonstrated need but they also boast an average net price of only $12,937 per year! That’s astoundingly low for a private university. Can the Peacocks spread their feathers once again? I’ll take them over Tennessee.

5. How about them Gators? Before you accuse me of being a brown noser and trying to ingratiate myself with my local readers, you should know that UF meets 98% of demonstrated need, and their average net price is only $9,809. Sure, most of their discounting comes from the Bright Futures scholarship, which is actually state merit aid and is funded by our collective Florida Lottery addiction. But I cannot turn away from those numbers – in the State University category, only UNC and UVA can boast higher generosity levels. So I’ll take the Gators to advance all the way to the Elite 8, where they will run into powerhouse Duke, a school with great basketball and financial aid tradition.

Take a look at my 2024 University Generosity Bracketology below. Spoiler Alert: My Final Four includes Yale, Duke, UNC and…St. Peter’s.

Let the Madness begin!

Best, Peter

P.S. If you want to understand University Generosity specific to your family’s financial situation, feel free to connect with us and let’s take a closer look.

P.P.S. Important Disclaimer – I take no responsibility for your own personal bracket. Make your selections at your own peril! My university generosity picks have nothing, and I mean nothing, to do with the game of basketball, so please don’t blame me if your selections fail. I grew up playing basketball and know a thing or two about the game. But I also know that the winners of these bracket pools often end up being people who select teams because of the nicknames, the school colors, the weather, or they have friends who went to a certain school. Two years ago, the winner of my family’s pool was a big Wizard of Oz fan. Since Dorothy hailed from Kansas, she chose Kansas for that very reason, and the rest is history. Doesn’t seem like a winning formula, but that’s what makes March Madness fun, right?

Earlier this week Dartmouth College, that esteemed Ivy League school located deep in the New Hampshire hinterland, announced that it would end its test-optional admissions policy starting with the incoming Class of 2029 (11th graders – that’s you!).

In their announcement, Dartmouth cited new research linking performance on standardized test scores to performance on campus and improved diversity and equity. We can certainly debate the merits of those findings — and I’m sure many scholars will — but that will not change how this announcement will alter the college admissions experience for your college bound teen. Yes, I do expect many other schools to follow Dartmouth’s lead.

Research aside, Dartmouth’s decision is at least partly a pragmatic response to what ‘test optional’ has done to Admissions offices… namely, overwhelmed them with nearly indistinguishable applicants. The test-less movement enticed students with strong grades and extra-curriculars but perceivably sub-par scores to throw in their application to, say, Dartmouth, believing they had a chance despite their lower than average scores. Multiply this by several thousand and we understand the unbelievable surge in the volume of applications.

This increase in applicants was a welcome and intended consequence of the schools’ boards of directors (the more applicants, the more selective the school appears, the higher the ranking). We’ve been tracking and writing about the Test Optional movement for years. Not being able to fairly or efficiently evaluate applicants without the additional benefit of a universal metric (like a test score) was an unintended one. Admissions offices have not been properly equipped to manage the deluge. (See also my article about high number of deferred applicants)

Fact is, standardized testing has always been critical to the admissions process. Most ‘test optional’ schools still invited students to submit scores, in fact they encouraged students with scores above the school’s average to submit them (test scores, like the above-mentioned selectivity, factor into a school’s ranking).

I’m sure the folks at the College Board and the ACT were popping the champagne at this recent announcement. If the College Board were a publicly traded company (instead of a very wealthy nonprofit) their stock price would have blown through the roof on Monday. I expect that more schools will follow Dartmouth’s lead and make similar announcements in the weeks ahead, especially if they buy into the research that the testing requirement can lead to more campus diversity in a post-Affirmative Action world. We would expect these announcements soon, as the Class of 2029 is about to enter the heart of their heaviest academic lifting period and testing cycle.

What would keep schools from quickly following Dartmouth’s lead is the school’s need to balance their desire for more applicants with the practicality of requiring a standardized test score in evaluating otherwise similar applicants.

Notably, there were hundreds of schools that adopted test-optional admissions policies well before Covid necessitated it. I expect these schools will remain test-optional well into the future and include many of the smaller liberal arts schools, but also major universities like University of Chicago, George Washington University, Wake Forest and American University. The University of California System went beyond test optional to go test blind – they don’t consider test scores at all in their admission decisions, a policy that is likely to remain for the foreseeable future. Meanwhile, in Florida, the state schools have always required test scores and will continue to do so.

Clearly, if you are in 11th grade or younger (or the parent who loves one of these bright young scholars), it’s time to prepare for a new reality where testing will be required once again at many of the schools that dropped the requirement during Covid. Your test scores will (at least should) help inform your admissions and funding strategies. A strong relative test score can not only benefit your admissions chances, but it can also lead directly to institutional merit scholarship dollars. You’ll need to have a good testing strategy, which involves knowing which test to take, when, if/when to take it again as well as ensure that you have the right preparation and tutoring.

Just another thing to add to your college preparation list! To that point, I’m going to be hosting a webinar with Admissions representatives from a cross-section schools that both require test scores and those that don’t. We will be discussing a number of topics including how Admissions officers utilize test scores (or don’t) in their evaluation of an applicant. The program will be in mid-March and will have limited ‘seating’, so stay tuned for your invite.

Happy Wednesday and Welcome to our first College Concierge Gift Guide!

With Valentine’s Day a week away, we thought it was the perfect time to share some last min ideas for the college and college-bound students you love.

For the past 18 years, we’ve been sharing our strategies to help you find and pay less for the right colleges. With literally thousands of students using our programs to get to and through college, we also know a thing or two about how to help them make the most of their experience while there. In that spirit, we are very excited to start bringing you some fun, new content to help you help them better navigate life on campus.

Hope you LOVE these Valentine’s ideas as much as we do.

Makeup Sponges If your child is going to wear makeup, there’s no better way to remove it than with these heart-shaped, facial sponges. They are made of 100% natural sponge extracted from wood pulp and environmentally friendly.

BAND-AID No matter how old your child is, a boo boo is a boo boo. These heart shaped band-aids are the perfect gift to put a smile on their face when they get a paper cut, scrapes or scratches.

KIND LIP BALM Great gift for boys and girls! KIND Lip Balm ensures your lips not only stay hydrated, but also enjoy the sweet treat of natural and delicious flavors. Used with natural ingredients and Made in the USA.

COOKIE CUTTER Baking in college just got a whole lot sweeter. Fun way for your college kids to enjoy making cookies, pancakes, treats and more.

MRS. FIELDS COOKIES If you child doesn’t want to bake their own cookies, then one of our favorite ways to say Happy Valentine’s Day is with Mrs. Fields. All of their friends will love your for sending this, too!

MISSING YOU LIKE CANDY They say that “absence makes the heart grow fonder”, but being away from you is not easy. You’re always the best “hi” and hardest “goodbye” so here is something for you! Made of natural soy wax.

COZY SOCKS Nothing says “college cozy” like these fleece lined socks. Perfect for hanging around the dorm or apartment. Your child will be so comfy he/she may actually enjoy studying!

READY FOR YETI Who doesn’t love a good water bottle? Yeti is the pinnacle of performance and your college kid can never drink enough water. So many fun colors to chose from!

Apple AirPods Gen 2 – For the apple of your eye! The Apple noise cancelation earbuds are perfect for any college student to keep out the noise. Definitely worth the investment.

In a normal year, the government rolls out its new FAFSA application in October. We prepare and submit the requisite financial aid document(s) on behalf of many of our students, much like an accountant prepares a tax return; and then, that information is forwarded by the DOE (within 2-3 days) to the colleges we’ve indicated. Our applicants then receive their financial aid ‘offers’ around the time they receive acceptance notifications, which in turn, gives us sufficient time to evaluate those offers, and should we deem appropriate, ‘negotiate’ them. Not this year.

Here’s what’s happened.

First, the government made fairly significant changes to the Title IV regulations governing financial aid calculations (you can click here to read about the implications of those to your family). Then, in an effort to ‘streamline’ the financial application itself, the government overhauled the document(s) which delayed their launch of the new FAFSA by nearly three months. It finally went live on December 30 and it coincided with an announcement by the Department of Ed. that (likely due to ‘bugs’ in the new forms) they would be holding onto applicant data until the end of January. While this definitely impacted the typical timeline that colleges required in order to make offers, it likely would not have affected our students’ abilities to make decisions — and put down deposits — prior to the May 1 decision day deadline most universities adhere to.

But then…

This week, on January 30, the Department revealed the disappointing news that they would have to further delay forwarding student information until March.

The Department of Education announced this week that FAFSA applicant information would not be transmitted to colleges until the first half of March. The primary reason cited for the delay is an error in the formula related to income tables that were not adjusted for inflation. The new formula was created back in 2020-21 and did not account for the recent rise in inflation that far surpassed previous economic trends. Hence, a greater portion of a family’s income was left unprotected, an error that could cost some families thousands of dollars in potential federal grants.

Thus in some ways, I’m glad for the delay. The government’s failure to bake in the past two years’ rapid rise in inflation would likely have disproportionately impacted many of my clients, and many families throughout the country. That said, this week’s announcement came as a surprise and, in some cases, a shock both to the admissions and financial aid offices who are waiting for this data to make offers to recently admitted applicants, and to parents of high school seniors who will likely be pressed to make quick decisions on where to enroll their children by the May 1 deadline.

If you’re the parent of a 12th grader you should know and do the following:

1. When you (or your aspiring college student) log into the various applicant portals, you will likely see that your FAFSA remains missing, even if you have already completed the form(s) days or weeks ago. Do not worry – given the above, this is expected. And while it may create some current consternation, the bigger challenge is coming later this spring when colleges will be scrambling to assemble appropriate awards. On that point…

2. Families typically have at least a month, often more time, to evaluate awards, ‘appeal them’ (read here what that means), and decide on a school by May 1. But this year, some schools will not be able to distribute award notifications until much later than April 1, perhaps just prior to May 1 or even afterwards. As a result, there is A LOT of pressure on universities to extend the May 1 deadline. On Wednesday, nine higher ed organizations (including the National Association of College Admissions Counseling, of which I’m a member) called on colleges to officially extend their May 1 for students to make decisions. I expect most will offer some flexibility, if not outright extensions. And for the prepared students (see below), I think there will be significant opportunities. So,

3. Make sure that you control what you can control. What I mean is that regardless of the government’s delays, be sure that you have done everything required on your end (with no errors). Make sure your FAFSA, and if required the CSS Profile, as well all supporting documentation, have been submitted properly.

4. When required (and only when required), send your tax return info to the colleges who are asking for it. If they don’t ask, you should not send.

5. It helps to know your estimated Student Aid Index, as well as the historical generosity levels of the schools on your list, so that you can at least ballpark what you can expect from specific schools. We have software that we use to project very accurately what each family should expect to receive from every school on their list. This pre-planning will help tremendously when dealing with a condensed window for evaluating and requesting ‘more’ from the schools you’re considering.

Which brings me to my last point, which I’ll direct to parents of teens in 10th and 11th grade. The government utilizes the income and financial data from the calendar year of 10th to 11th grade. In other words, any adjustments you make to benefit (or hurt) your chances for institutional grants should be made before January of 10th grade. That’s why we like to begin working with our families in 10th grade at the latest. When we do so, not only can we accurately estimate your student aid index (what they’ll say you can afford to pay for college), we’ll also be able to recommend meaningful adjustments in time, and if applicable, to reduce what they say you can pay (thereby increasing what the colleges on your list will ‘give you’ to bridge the gap).

So, moral of the story: we/you cannot control the government’s schedule, or rollout, or delay, or legislative whims or inflation, for that matter. You can, however, exercise some control over your ability to plan ahead and take full advantage of any and all of the above. As always, if you have any questions about your family’s opportunities to pay less for colleges you’re considering — or which colleges you should be considering so that you can pay less, please feel free to reply to this email me at info@yourcollegeconcierge.com, or give me a call, 954-659-1234.

March Madness is around the corner, and with it comes my 15th annual University Generosity Bracketology. So I’m going to get right to the point.

Some colleges are generous.

Some colleges have strong basketball programs…

…and some colleges are both generous AND have strong basketball programs.

Why does all of this matter? There are two reasons – one is critically important, and the other is, well, trivial but fun.

In my 15+ years of guiding high school administrators, students and families, the issue of affordability is often central to the conversation around assembling a list of colleges. It’s no secret that the cost of attendance (COA) at both private and public universities has been on the rise. Back in 2007, when I began advising families, the average COA at a private university was (only) about $56,000 per year; that number is closer to $80,000 today and still on the rise. I just spoke with a family whose daughter was admitted to NYU. Their COA at the Tisch School is a whopping $93,132 per year! However, most families we work with will pay far less than the COA.

Remarkably, the COA at state universities, especially here in Florida, has only increased slightly to about $23,000 annually. State costs have risen steadily across the country, but not at the same level as private college costs. But that’s only half the story.

What is less understood is the way colleges “discount” by offering need-based or merit-based aid, or a combination of the two. In fact, all colleges offer discounts, just not in the same way or at the same level, nor do those discounts apply across the board to all students. What is of critical importance to you and your family is to know: 1. which colleges are likely to offer a discount to you; 2. whether that discount will be in the form of need-based or merit aid; and 3. how you can maximize your chances at either or both.

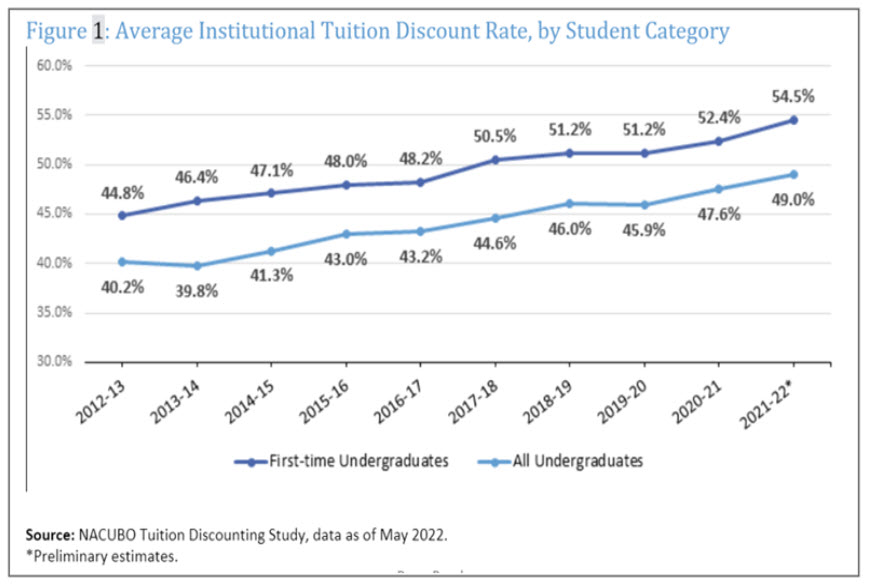

Just looking at the numbers below from the National Association of College and University Business Officers (NACUBO), tuition discounts have been on the rise for several years, approaching a whopping 54.5% during the 2021-22 academic year:

These numbers largely reflect merit discounts, or awards based on grades, test scores, and other factors based on high school performance. Truth is, many colleges offer discounts as a strategic incentive to lure students to enroll.

In brief, the merit discount strategy works like this:

Colleges charge a high price so that the public perceives an intrinsic value. Then, they will offer a big “scholarship” (read: discount) which makes both student and parents feel good and will make the student more likely to enroll. The amount of the discount may vary based on academic performance, but it also might be a way to target students from specific socio-economic backgrounds, high schools, or zip codes. After the discount the remaining cost is still significant so that the school enjoys an impressive sum, but it’s low enough that mom and dad can figure out a way to pay. And, they can tell all their friends that their brilliant child earned a scholarship.*

The other way that schools discount is by offering need-based aid to families who demonstrate financial need on the FAFSA and the CSS Profile. The calculation for need-based aid is more direct and transparent, though changes to the federal formula in the next admissions cycle (2023-24) will result in some confusion for many families. Still, most schools publish the amounts they award, on average, as a percentage of the need. So if a school meets over 80% of the demonstrated need (there are many of them!), we would consider that to be quite generous.

There are about 70 colleges who meet 100% of the demonstrated need. You might conclude that these schools are particularly generous, and therefore you should apply to them to get the best financial aid package. But that depends on your own family’s income and net worth. An Ivy League school will appear super generous to a family earning less than $100,000 per year, but that same Ivy will offer exactly $0.00 in merit aid. So, for families earning in excess of, say $300,000, an Ivy League school isn’t generous at all. This is one reason why students should apply to schools that are right for them, not only academically and socially but also financially, as opposed to selecting the same colleges that your friends are applying to.

So what does this have to do with March Madness? Long time readers may recall that each year I take a look at the Men’s Division 1 basketball bracket of 68 teams, and I apply my own “University Generosity” formula to predict the winners. By doing this, we can see how schools differ in their degree of generosity. My methodology may not win you much money in your office pool, but it could yield incredible gains in terms of scholarship and need-based aid when your child receives his/her acceptance letter in April of 12th grade.

Selection Sunday is next weekend, March 12. Next Tuesday, March 14 I’ll be announcing my #UniversityGenerosityBracketology bracket live on Facebook, at approximately 12 pm ET. I’ll send a Live link before the event, you can follow us on Facebook at www.facebook.com/yourcollegeconcierge.

No athletic event gets me quite so excited as March Madness. The Cinderella stories, the buzzer beaters, the upsets – every March this event always delivers. So I figure, let’s try to learn something about these colleges and their generosity in the hope that it will aid in the process of selecting colleges for your child. Come and enjoy the excitement with me, and let’s identify the most generous colleges among the 68 lucky dancers, er, participating teams.

If you would like more insight into the college admissions or financial aid processes, don’t wait until the last minute when your child is already in the midst of his/her senior year. The best plan is an early plan – reach out to me at peter@YourCollegeConcierge.com or call us at 954-659-1234 to learn how we might be able to assist you and your child with this exciting yet complex exercise that is college admissions.

Here’s a little something that many of our newer readers are surprised (in a good way) to learn. Unlike typical admissions decisions, the financial aid offers that accompany your admissions letters are far less final. With financial aid, you have more room to maneuver, to appeal, even (gasp!) to negotiate a stingy offer than you do an unfavorable admissions decision. Notice the language difference: admissions decisions, and financial aid offers.

The latter can be countered, as in you can make a counter-offer, request to ‘be reconsidered’, or appeal for more money. And here’s the best part. Quite often, when done so correctly – you’ll get more. Sometimes quite a lot more.

So, should you be appealing your financial aid offer? Well, that depends (which I know is annoying, but it’s also true). Actually there are many good reasons to appeal a financial aid offer, but first and foremost, you have to determine if the offer you have received is fair (as in, is it consistent with both the school’s stated financial aid policy and it’s historical practice).

The first thing I do when presented with an award letter is calculate how much the student deserves to receive. This way I have a benchmark to compare the award with, instead of merely crying “it’s not fair!”

How do you calculate a “fair” award? By applying the financial aid formulas and researching what percentage of financial need the college meets.

The financial aid formula is: Cost of Attendance – Estimated Family Contribution = Need.

Cost Of Attendance means how much it takes to send your child to school for one year – tuition, fees, room and board, books and supplies, travel expenses, insurance, and so forth.

Estimated Family Contribution is an amount that the government determines that you can afford to pay each year. It’s derived from filling out the FAFSA and in some cases, the CSS Profile.

(Most families are unhappy with their EFC because government formulas often have little relevance to a specific family’s financial circumstances. For example, a family of 4 with an adjusted gross income of $150,000 and one student in college will have an EFC of about $30,000, or approximately 1/5 of their income. There are ways to reduce your EFC, but that takes advanced planning of a year or two. So the best time to start is when your student is in 10th grade or earlier).

So if Cost of Attendance is $80,000, EFC is $30,000 you will show financial need of $50,000. (COA-EFC = Need).

The next step is to research how much need the college says they’ll meet and how much they have historically met. All schools discount to some extent. Perhaps your child’s dream school is a generous one, and meets 90% – in this case $45,000, leaving only $5,000 unmet.

I realize your eyes could be glazing over right now, so I’ll stop with the calculations.

But if you’re still following, we just figured out that a fair award is $45,000. If you receive that amount or more, I would not bother appealing, but it depends on the allocation (grants vs. loans and work study). If you receive less than $45,000, I would question the award and consider an appeal.

Now, all of the above assumes that the financial aid applications the family submitted did not contain any errors that may have inadvertently inflated the family’s expected contribution. Many applications do contain such errors, and these can be costly. But they can also be addressed, explained, and/or appealed.

Perhaps, for example, upon review, we realize that you have accidentally inflated the value of your small business by using an IRS standard as opposed to the Dept. of Ed. formulas. Or perhaps, you included the value of the 529 your parents’ purchased for their grandchild or worse, you misclassified this asset as a student asset (note: student asset are more heavily penalized in both the federal and institutional financial aid methodologies). In those cases, we submit corrected applications along with an explanation for the changes. I’ve seen cases were retirement accounts or home values are included in assets, and this, too, can be unnecessarily costly.

We’ll also appeal on behalf of families who may have experienced a change in life or financial circumstances that is not reflected on the financial aid applications (note that the financial aid applications are using data from January of your high school child’s sophomore year to December of their junior year — and things do change). We’ll request reconsideration for an award if the family has experienced a job change, a medical issue that results in high expense or time away from work (lost wages), a natural disaster, or some other event that has a significant financial impact.

The best way to appeal is to write a letter to the financial aid office and copy the admissions person who signed your child’s acceptance letter. Admissions has a vested interest in having your child say ‘yes,’ so keep them in the loop. Some schools have institutionalized the appeal process, with websites explaining their process and specific forms to complete. You’ll want to follow their rules and procedures, or you’re simply wasting your time.

Make sure that you are both thankful and positive in the letter – tell them how much you appreciate their original offer (even as you are about to ask for more!). Describe how eager your child is to attend this prestigious school. Then mention that, as it stands, what they have offered is not enough for your son or daughter to be able to attend. If you can demonstrate that you were under-awarded, do so here.

If you have background about your finances or other relevant information that did not show up on the initial financial aid forms, this is the time to explain it. And don’t be afraid to use emotion to paint a vivid picture for the financial aid officer, who, for the most part, tends to be an actual human being with feelings!

If you were laid off, describe not only the financial impact but also the pain and suffering that you experienced. If you’re self-employed and your business suffered a downturn, this letter is the place to demonstrate it and make the reader feel that they’re right there with you.

Before you ‘appeal’, you should probably wait until you have received all of your ‘offers’. That way, if you received a more compelling award from a competing university, you can mention it! Sometimes (not always), you can use it to play one school off the other, particularly if you can honestly say something along the lines of “Your fine college is Charlie’s first choice, but he received $12,000 more in grants from Faber College. If you can come close to matching Faber, he’s coming to your school!”

One cautionary note – don’t bluff! You’d better be able to prove that you were offered a better award package elsewhere, because you may be requested to produce it. And finally, make sure you call it an “appeal.” Never use the word “negotiate” – the theory (still unproven) is that financial aid officers think that word is too transactional so to be safe, stick to the more academic ‘appeal’.

If you’re the parent of a 12th grader who is currently reviewing your financial aid offers and would like more in depth information, check out this podcast Carla and I recorded a couple of years ago. If you still have questions, you can send me an email and perhaps we can improve your offer.

As always, thank you for following our content and allowing us to help support students and their success!

Faced with what The Wall Street Journal once called a ‘mind-numbingly complex’ process of evaluating 4000 universities and determining which are the ‘best’, families often turn to independently produced and widely-touted but rather dubious indices and rankings systems (yes, US News, I’m talking ’bout you).

I have so many students who, when they’re first building or paring down their college lists (which we’re doing right now with our sophomores and juniors), will point to the rankings and say that they’ll only consider the top schools, which presumably are the ‘best schools’.

My response is often: Rather than consider what’s ‘best’, let’s look at what’s ‘best for you.’

Let’s start, for example, with identifying schools that offer academic programs, or majors, you’re interested in pursuing. My alma mater, Tufts University, is currently ranked #32 by US News, but you can’t take a single business class there. Is that a better choice for a DECA kid who is keen on studying business than #41 Boston University? or even #44 Case Western Reserve University? Probably not.

Now I’m not against using data to inform your college planning decisions. Data can be very useful. It’s just that ‘rankings’ are just a starting point. They are not an absolute.

As a whole, the rankings like those in US News do offer a singe place where data on schools is collected. And when that data is deconstructed, students can learn some interesting things about the schools they’re researching. But, when rankings are used as whole-scale evidence that the 15th ranked school, Washington University of St. Louis, for example, is ‘better’ than the 25th ranked school, New York University, there are real problems. There is nothing geographical, cultural or academic that makes it possible to really compare these two universities and assign a generic ranking that determines whether one is better for your child than the other. Fit matters – academic, social and financial!

In an effort to address these issues (and, let’s face it, to compete with the aforementioned rival media outlet, US News), the NY Times recently introduced a ‘Build-Your-Own’ rankings tool with 900 colleges and universities in its database. It’s an interesting endeavor with an appealing premise — and you can try it here. My concern is that any ranking system based on an individual student’s preferences is actually far messier — and thus less reliable — in execution than it is in its intent. That’s because many of the data points utilized to feed the algorithms include factors like post grad earnings of former financial aid recipients and racial diversity. These are measurable considerations but not exactly quantitative in that they are subject to the human interpretation of the people feeding the system. Like most any data, rankings data might be ‘numerical’, but not exactly objective.

So, how do you build a ‘perfect list’ of colleges? First, be mindful that there is no optimal list that applies to all. There is, however, an optimal process by which to build that list. And that process starts with each individual student identifying preferences (academic interests, high school performance, career aspirations, campus lifestyle, location and locale, student organizations, average class size, etc.), while taking into consideration the family’s ability to pay (budget, expected family contribution, financial aid generosity, availability of merit scholarships, etc.). Then it moves to looking at the schools that can meet those criteria.

The list-building process should be initially inclusive (think 40 schools to be researched in 10th/11th grade). And then a good college list is one that is ultimately focused, intentional and strategic (think 12 max by the summer before 12th grade).

Remember to consider the financial realities and make sure you understand your family’s Expected Contribution and your particular talents/achievements so that you can anticipate the level of discount you’ll receive from each school you’re considering (We utilize software that can accurately project this in advance). Nothing is worse than including schools on your list that you categorically won’t or can’t attend. And finally, recognize that a large majority of any applicant pool will meet the school’s requirements – this is competitive – so make sure you build a list with a mixture of reach, target and likely schools from an admissions and financial basis.

As we move into the final stretch of this academic year, we begin to focus in earnest on making sure our 11th graders are positioned to submit their applications BEFORE they get mired in the academic crush and pressure of 12th grade. This includes making sure that each student has the right colleges on their list!

If you’re an 11th grader (or a parent who loves one), there are steps you can be taking now to ensure that the entire application process goes smoothly – without the needless stress that comes with doing things late or without the proper guidance. We like to say, to get ahead it’s good to get a head start!

And with that in mind, we’re opening our early bird registration for our 17th Annual Summer College Admissions Bootcamp. This is a 6-week program with live instruction and one-on-one office hours. We guarantee that every attendee will have a submit-ready college application (including a stand-out essay and activities list) BEFORE the start of the next school year.

You can review the syllabus here – and if interested, register your child today. Please keep in mind that this program is guaranteed to all of our Gold/Platinum clients at no additional charge and has sold out to the public every year. We often have a waitlist of students, so be sure to register your rising 12th grader and avoid being on the outside wishing your child enjoyed the necessary support. We hope to see your soon-to-be rising 12th grader in our class!

Again, check our our syllabus by clicking here – and feel free to shoot me an email if you have any questions about this program – or any other component of the college planning process. I know it may appear daunting right now, but I promise that with the right support, it need not be!!

Today is ‘Decision Day’ for our college-bound high school seniors (and the parents who love them). May 1 is the day that the deposits are due, and let’s just say it can be an equal parts anxiety-inducing and euphoric day. Mostly euphoric we hope, but the day can be anxiety-inducing for many because this year has been yet another record-setting year for low acceptance rates among the ‘top’ (read: popular) colleges. More schools than ever are reporting single-digit admit rates – schools you may have not considered ‘selective’ even 5 years ago. NYU, for example, is reporting that they received more than 120,000 applications – and accepted only about 8% of those. UPenn also claimed a record number of applications – 59,000. As did Dartmouth with nearly 29,000 applications. Duke had over 44,000 applications and accepted only 4.8% of them. Fueling this madness are the usual suspects: unrelenting marketing by colleges with a healthy assist from a number of ‘nonprofit’ educational services (like The College Board, to name one). There’s also more and easier ways to apply to multiple schools than ever before. And then there is the sad truth that there’s an appalling lack of access to college guidance (national average is 502:1, as in 502 12th graders to every college counselor).

The result? We see a growing number of high school students (and the parents who love them) who are finding themselves adrift, reflexively applying to dozens of colleges regardless of fit, spreading themselves thin and failing to do the ONE THING that can actually move the needle on this whole process.

Though there will always be a lot of uncertainty inherent in College Admissions, the fact remains that ultimately, the decisions are still made by people. We’ve been saying this for over a decade. In that time, technology has advanced, applications have changed, tests have been overhauled…and yet, there remains one constant in the Admissions and Scholarship Process. It’s that with the right strategy – and more importantly – with the right execution of that strategy, your child can positively influence the outcome.

From an admissions standpoint, please understand that nearly all colleges will be rejecting legions of qualified applicants – MANY of whom would have been admitted just a few years back.

In fact, back when most of today’s parents were applying to college, it was rare for a school (even the Ivies) to accept fewer than 20% of its applicants. Today, there are many schools with single digit admit rates! And they are all ‘proudly’ setting (and celebrating) new record low acceptance rates. And many, many more will admit between 10 and 20% of applicants, including schools you might not expect.

This is happening despite the fact that overall college enrollment reached its peak in 2011.

This news shouldn’t surprise any of our clients or our readers– we’ve been reporting on and preparing our students for these type of long odds for 17 years.

One irony is that while college admissions has become increasingly competitive, the tuition discount rate (the amount of institutional grant and scholarships offered to admitted students) has reached a record high of 56%, according to the National Association of College and University Business Officers (NACUBO). Yes, that means that we expect most of our students to pay LESS than half of the published price for their college education (which can equate to literally tens of thousands of dollars).

These types of outcomes and opportunities do not happen without a proactive and strategic effort. For years, we’ve emphasized the importance of niche positioning when it comes to standing out in a crowded Admissions and funding process. That’s because despite the mania, the college process remains a very ‘personal’ one, managed by real people who are moved by emotion and subtleties that are not reflected in scores, GPA or class rank. What separates two seemingly identical students on paper are intangibles – what we call an ‘X’ Factor.

In our practice, we develop an individualized and targeted Admissions strategy for each of our families. During high school this allows the student to shut out the noise and work on their plan…and when the time comes, they resist the pressure to defensively submit applications to ‘cover their bases’ and instead focus on building their case before a list of 8-10 schools that we know will consider their value (be it academically, socially or even geographically) and be capable of meeting the entire family’s needs.

The truth is that while there is now more information available than ever – including various school rankings, net cost calculators, ROI estimates, etc., the process is becoming more daunting and confusing than ever. This need not be the case for you and your students. There are 4000 universities and many right options for each child and budget. The goal is to identify those that meet your family’s needs and implement a strategy well before your child hits submit on their first application.

In just over a month, we’ll begin oursummer Application Bootcamp for rising 12th graders (current 11th graders). In that 6-week program we will be working with each student to fine-tune their college lists and admissions strategy, create a killer college application and write a unique essay that will ensure that their application gets the attention it deserves. Every single student who participates is guaranteed a submit-ready college application prior to the beginning of 12th grade.

This is the 17th year we’ve offered this program and past students who have participated have been able to receive their first ‘yes’s’ early in the Fall. You can click here to see our 6-week syllabus and/or to register your 11th grader. Note – this class is guaranteed for our Platinum and Gold clients and it does fill up – we usually have a wait-list so if you’re interested, reserve your student’s place today.

P.S. One way you can judge the results of our program is by the number of options our students get to choose among. So with our heartfelt congratulations to our seniors and their families, here is a sampling of the places our students are heading next fall.

Babson College Brandeis University College of Charleston Cornell University Dartmouth College Elon University Embry Riddle Emerson College Florida Atlantic – Wilkes Honors College Florida Institute of Technology Florida International University Florida Polytechnic Florida Southern Florida State University Georgia Tech Indiana University Marist McGill University New York University North Carolina State Notre Dame Nova Southeastern University Ohio State Penn State Purdue University Reed College Skidmore College Southern Methodist University Texas A&M University of Central Florida University of Florida University of Illinois University of Maryland University of Miami University of Michigan University of Pennsylvania University of South Florida Virginia Tech Wellesley College

In 17 years of helping students and parents navigate the college admissions and financial aid landscape, I have personally prepared and submitted around 4,000 financial aid applications. During that time, there have been a few, relatively minor tweaks to the main financial aid application – the Free Application for Federal Student Aid. Well that’s about to change.

What we are about to see with the next admissions cycle (2023-24) and, in particular, the changes to the Title IV financial aid rules, represent the most significant change to higher ed access in years. Parents of current 11th graders and younger students should pay close attention.

A few years ago (December 2020) Congress passed the FAFSA Simplification Act, a piece of legislation that was long in the works and was attached to a Covid relief bill. The new rules incorporated in that law are scheduled to take effect in the Fall 2023, impacting the academic year 2024-25. Like most legislation, if you know the loopholes and the landmines inherent in the rules, you can greatly benefit. If you don’t, there is a much greater risk you’ll needlessly suffer. Below are some highlights – including our researched analysis of its likely impacts.

1. The FAFSA will be simplified (hence the name of the law), with questions reduced from 108 to 36. This is very good, and it should make it easier for families at all income levels to apply for aid and not be deterred by a complicated application. On the other hand, with fewer data points to feed the algorithm, it becomes even more critical that your application is completed/submitted sans any mistakes – particularly in the interpretation of what information is being requested (i.e., never ever identify a 529 or Prepaid plan as your child’s asset AND you don’t value your business in the same manner as you would on an IRS document or on a loan application).

2. Pell Grants should be available to more families. This is also good, making college more affordable to low-income families. Separate from the legislation, the maximum Pell Grant is likely to increase, benefitting the most needy families. That said, it’s important to remember that while Pell Grants offer the largest aggregate of grant dollars available, they are distributed in relatively small increments (currently the max Pell Grant is around $7,395) and are only available to lower income families (generally, AGI less than $60,000). Many of our readers and the families we work with will be unaffected by this change as they enjoy the largest discounts — as in sizable five figure scholarships – in the form of Institutional (not Federal) grants. At the ‘right’ schools, these are available to families with considerably higher incomes – even to those whose AGIs are greater than $200k.

3. The definition of “untaxed income” is changing, with the most common types no longer reported on FAFSA. Untaxed income is a traditional killer when it comes to financial aid, as these amounts are added back to a family’s income when calculating what the family can pay. Examples include 401K contributions and child support. While some untaxed income will still be reported, the definition is changing which will benefit many families, particularly those where child support is a primary source of income.

4. Colleges must be more transparent when disclosing their costs. Many families are confused by the published information about how much a school actually charges. Some colleges have been traditionally (and intentionally?) opaque when it comes to sharing their cost of attendance. Starting next fall, colleges must adhere to federal guidelines when disclosing how much they charge. It remains to be seen how well this new regulation will simplify the cost structure but I will stay optimistic for now.

5. For divorced or split households, the definition of a “custodial parent” is changing. This new rule may impact which parent is required to disclose financial information on the FAFSA, which in turn could negatively impact how much financial aid a student will receive. Prior to this change the FAFSA only required the financial data of the household where the child resided 51% of their time. The new law defines the custodial parent as the one who provides the most financial support. This definition may be subject to interpretation.

6. The new FAFSA formula no longer considers the number of students in the family who are enrolled in college. This is perhaps the most significant, most problematic and possibly the most devastating change, especially for middle and higher income families with multiple children attending college at the same time. Under the current rules, when families report income and assets to determine what they can pay, the federal formula divides that amount by the number of students who will be enrolled. For example, let’s say your family’s AGI is $150k and the FAFSA determines that you have an Expected Family Contribution of $40k. If you have two students enrolled in college then each contribution would be $20k, which makes sense. But that rule is going away, and you would be expected to pay $40k for each child. So, on the face, this change seems devastating… BUT… and it’s a big BUT… the CSS Profile (the Institutional financial aid application) is NOT changing this rule — and according to my sources, colleges who use the CSS Profile to determine institutional aid have no intention to follow the FAFSAs lead on this matter. Equally important, it is the CSS Profile (a very complex and intrusive financial aid form with about 250+ questions) and the colleges/universities that require it, that offer the highest amount of scholarship and grants! CSS Profile schools are also the most generous schools. So, net net when you apply to the right (as in generous) colleges, your opportunity to reduce the cost of your child’s education increases significantly.

And, the average ‘discount rate’ has reached an all time high of 56%, so don’t let these changes deter you. So, while sticker prices are rising and financial aid rules are making it more challenging for some families, the schools themselves (especially private ones) are still finding ways to offer significant discounts which allow middle class families more opportunities to afford what appear to be very expensive universities.

In fact, over the past 17 years, our students have received approximately $33,500 per student per year in institutional, federal and state grants. So, while there is most certainly going to be disruption in the financial aid system this coming year, it need not be a negative experience for your family. Financial aid is somewhat of a high stakes game in that when you know the rules – of both Title IV finance regulations AND college admissions, you know how to work those rules to your family’s advantage. When you don’t, you do risk missing out on opportunities and needlessly leaving thousands of scholarship dollars on the table.

For parents with current 11th grade students, we will be discussing these changes and exactly what you/your child can do to take full advantage of them during our summer application bootcamp. Specifically, we will be incorporating the changes and how it should impact your child’s college list during our Parent Orientation which will take place on June 15. As this program is guaranteed to all of our Platinum and Gold families we have limited seats still available. You can click here to see our syllabus and to ensure your child can participate.

As always, please call my office (954-659-1234) or send me an email if you have any questions about the new Financial Aid regulations or any other college planning question or concern.